Flow")

A Paycheck Check-Up To Embody Your (Cash) Flow

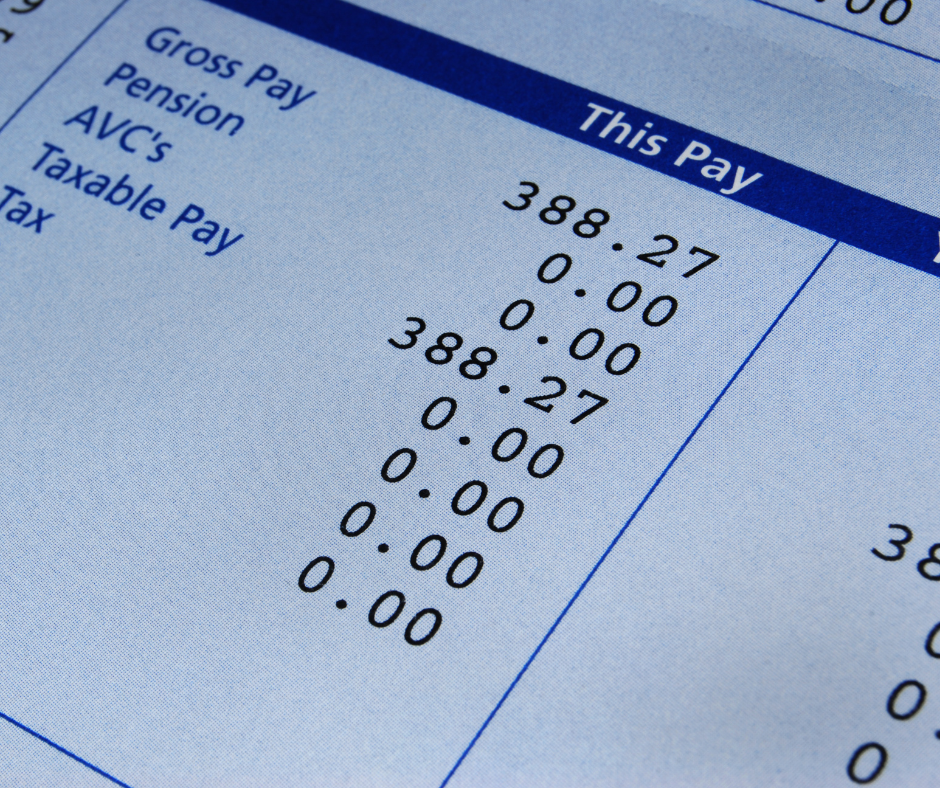

Committing to a routine paycheck check-up can help avoid headaches for some and cause anxiety for others. Understanding and reviewing your paycheck stub is both a matter of practicality and purpose because what we learn informs the most crucial piece of your cash flow puzzle: your income.

A Logical Approach

To do a useful paycheck check-up, we recommend gathering the last two pay stubs you received for review, analysis, and comparison using a logical 6-point approach.

Team Duncan’s Paycheck Check-Up List

□ Verify Personal Information: Ensure your name, address, social security number, and other personal details are correct on the pay stub.

□ Check your pay period: Determine whether your paycheck is for a weekly, biweekly, semi-monthly, or monthly pay period.

□ Review your earnings: Check the following components of your income:

□ Gross pay: This is your income before deductions and taxes. Confirm that your hourly wage or salary aligns with your employment agreement and verify the number of hours worked or days in the pay period.

□ Overtime, bonuses, and commissions: If applicable, ensure these amounts are correct and follow your employment terms.

□ Examine deductions: Review the various deductions taken from your paycheck, such as:

□ Federal, state, and local income taxes: Ensure the appropriate taxes are withheld based on your filing status and allowances.

□ Social Security and Medicare taxes (FICA): Confirm these taxes are withheld at the correct rates.

□ Retirement contributions: Verify that your 401(k) or other retirement plan contributions are accurate and that any employer match is included.

□ Health, dental, and vision insurance premiums: Ensure the correct amounts are deducted for your chosen insurance plans.

□ Other deductions: These may include life insurance, disability insurance, flexible spending accounts, and union dues. Verify that these deductions are accurate and agreed upon.

□ Calculate your net pay: Subtract your total deductions from your gross income to arrive at your “take-home pay” (also called your net income). Your net income is the amount you receive in your bank account.

□ Compare your net pay to your budget: Ensure that your net income aligns with your budget and financial goals. If your net pay seems lower than expected, review your deductions and tax withholdings to identify any discrepancies.

Heart-Centered Approach

Did this checklist make you nauseous? Deep breath….I recommend 4-7-8 breathing. Take a four-count breath in, hold it for seven counts, and exhale slowly and smoothly for an eight-count breath out. Repeat this 4-7-8 breathing four times to relax and center.

According to an NBC News article by Vivian Manning-Schaffel in 2017, “As many as 78% of American full-time workers are living paycheck-to-paycheck, and it is taking its toll on our health”. The article indicates there are many people making $100,000 per year or more who feel stress and anxiety that is bad for their health. More than half of these $100k+ earning individuals are also heavily in debt and feel like it isn’t feasible to have an emergency fund. The article mentions the American Psychological Association (APA) indicates, “financial stress is the top cause of stress for Americans. It’s a well-known, scientific fact that stress has many negative ramifications on your health.”

Yes. For many people, the idea of analyzing their income may cause anxiety. Perhaps you feel you aren’t paid enough for the work you do. Maybe you think you won’t understand what you see when you look at all the numbers. Have you stuck your head in the sand so you can go on thinking everything is fine and will work itself out? Perhaps you feel strapped for cash like many Americans, and looking at your pay stub is a sad, frustrating reminder you’d like to avoid. These feelings are normal but are irrelevant to the actual task. Please remember, your pay is NOT a statement about your worth or your worthiness.

Income reported on your pay stubs reflects an important component of your current financial flow. When we say we want to get into flow, we mean to be aware of a steady, continuous stream. Flow can be a state of consciousness; it can be like fluid, gas, or electricity moving through systems or the flow of a river to the sea. As it pertains to your pay stub, the stream of money flow is your incoming cash flow, allowing you to live your best life.

The exciting part is that you have the opportunity to give each incoming dollar a job and then release it intentionally (like a breath!) to pay for your needs (fixed expenses), to live your best lives (our wants), and provide you the wherewithal to save for the future (wishes). Understanding net income from your pay stub is the first and most important step in creating a budget or spending plan. Giving every dollar a job and sticking to your plan is an efficient, uncomplicated way to flow intentionally toward prosperity.

A financial planner can meet you where you are and walk you through a paycheck check-up. Whether this is a practical task to check off a to-do list or an emotional topic that brings up some anxiety, you can lean into the knowledge and experience of professionals to gain income clarity and create a plan for each incoming dollar.